Tuesday, November 30, 2010

CDE - Breakout of Triangle - $30 price target.

CDE has been on a tear and looking to further its gains.

Wednesday, November 17, 2010

Strategy Update: SOX + MU + Elliott Wave Theory

Pollux Technicals- Strategy Update: SOX + MU + Elliott Wave

I first wrote about the PHLX Semiconductor comeback in 2008 in The Other Commodity post, when the SOX was all but forgotten, staggering around the global market, lost, since 2000, while the great commodity bull market of the new century was literally rising from the earths crust with buildings as tall and as high as we have seen - and it was happening fast. But again, the SOX was lost, meandering in over-capacity, falling prices, decreasing margins - you know, the usual suspects. Then the financial crisis took shape and commodities cracked, and so did the SOX, further falling, and aiming for levels not seen since 2003 and 1998 - it was a here we are again moment. And that was it, the same moment that made you feel like you had been there before was the same moment that would never be seen again.

And two years later, the SOX has climbed from 175(a 10yr low) to 400, a whopping 128%, while the CRB Index only rose 62.5%, going from 200 to a high of 320 early November. Now, while I believe the CRB can outperform medium to long term, now is the time to start thinking about entry strategies to get back into semi-stocks. I still believe we are in the midst of a secular shift in this sector - the premise being that Semiconductors are today where commodities were in 2003-2004, according to Elliot Wave. Look at the CRB below and what its WAVE 1 and WAVE 2 looked liked.

CRB Index - Emergence of the Bull.

Here is the SOX index, which is in a WAVE 2 correction, and entering a WAVE 3 - the longest wave of Elliott Wave theory.

SOX Index - Emergence of a Bull.

What are the factors driving the SOX?

Well, inflation is one of them(lower dollar), along with a consolidation in manufacturing and outright bankruptcies during the global crisis. Add that to demand globally, as the middle class continues to surface in emerging markets, which compensates the overcapacity issues, and there is a solid case for continued demand for electronics, and also alternative energies and its consumption of semiconductors. As the DRAM prices have stabilized over the past 2 years, we can see on the DRAM Exchange, that prices have retreated in the last couple of months, but have been on a rapid rise over the course of two years, bouncing hard off its 2008 historical lows. With the recent pullback in DRAM and FLASH prices, I believe that now is the time to start looking at semi-stocks again for the Long-Term - buy and forget about them mentality. You don't buy Semi stocks when DRAM/Flash drive prices are high, you buy them when they are low. I would start aggressively accumulating Semi-Stocks over the course of 1-3 months. According to the Elliot Wave Theory, the Wave 2 selling could be coming to an end.

I was bullish on Semi land up until Jan/February of 10, when I called for a 15%-25% correction in the blog posting Watching The Leaders For A Shift. It was also this time I grew a bit bearish on the market because Semiconductors are part of the leaders in the business cycle. I was then implementing a long late cycle/short early cycle stance for hedged protection in the The Exit Strategy post and so far the strategy has worked, as we have seen late cycle commodities moving higher while semis/banks have been lackluster, with downward pressure - and that why its time to get back to Semi land, searching for entry points.

Below is a chart of MU and an Elliot Wave analysis for re-entry into that stock - overall I would be patient and wait for strategic entries back into semi-conductors, but this is where the value could be hiding, and possibly even creating superior returns to commodities for the long-term. Knowing Semi's may be in the beginning of a secular bull market, a new hedge could emerge in using Gold as a short hedge. This though would require a bit more research, as for now the Gold bull is alive and well, and juniors still present undervalued opportunities. So for the long haul, we could be setting ourselves up for a Short Gold/Long Semi strategy, at some point, but I'm not about to go there just yet.

I will also include a Mean Reversion charting technique I use to give myself another form of methodology of where/when to enter into a position.

Why Semis? And why MU - besides the fact I like the way it trades and its large liquidity, it is easily to identify its pullbacks due to its very simplistic elliott wave formation. But also, as the dollar falls, our semiconductor products and pricing become more attractive, globally. As the dollar continues to fall, or even if it stabilizes, it will be a large factor in its global competitiveness. And in the end, Semiconductors are - The Other Commodity - and remember commodities make roads and buildings - chips make everything else.

SOX COMPONENTS

ALTR,AMD,ATHR,BRCM,CREE,CRUS,HITT,INTC,KLAC,LLTC,LRCX,SNDK,STM,TER,TXN,VECO,NVDA,MU,NSM,POWI,RBCN,STM.

I first wrote about the PHLX Semiconductor comeback in 2008 in The Other Commodity post, when the SOX was all but forgotten, staggering around the global market, lost, since 2000, while the great commodity bull market of the new century was literally rising from the earths crust with buildings as tall and as high as we have seen - and it was happening fast. But again, the SOX was lost, meandering in over-capacity, falling prices, decreasing margins - you know, the usual suspects. Then the financial crisis took shape and commodities cracked, and so did the SOX, further falling, and aiming for levels not seen since 2003 and 1998 - it was a here we are again moment. And that was it, the same moment that made you feel like you had been there before was the same moment that would never be seen again.

And two years later, the SOX has climbed from 175(a 10yr low) to 400, a whopping 128%, while the CRB Index only rose 62.5%, going from 200 to a high of 320 early November. Now, while I believe the CRB can outperform medium to long term, now is the time to start thinking about entry strategies to get back into semi-stocks. I still believe we are in the midst of a secular shift in this sector - the premise being that Semiconductors are today where commodities were in 2003-2004, according to Elliot Wave. Look at the CRB below and what its WAVE 1 and WAVE 2 looked liked.

CRB Index - Emergence of the Bull.

Here is the SOX index, which is in a WAVE 2 correction, and entering a WAVE 3 - the longest wave of Elliott Wave theory.

SOX Index - Emergence of a Bull.

What are the factors driving the SOX?

Well, inflation is one of them(lower dollar), along with a consolidation in manufacturing and outright bankruptcies during the global crisis. Add that to demand globally, as the middle class continues to surface in emerging markets, which compensates the overcapacity issues, and there is a solid case for continued demand for electronics, and also alternative energies and its consumption of semiconductors. As the DRAM prices have stabilized over the past 2 years, we can see on the DRAM Exchange, that prices have retreated in the last couple of months, but have been on a rapid rise over the course of two years, bouncing hard off its 2008 historical lows. With the recent pullback in DRAM and FLASH prices, I believe that now is the time to start looking at semi-stocks again for the Long-Term - buy and forget about them mentality. You don't buy Semi stocks when DRAM/Flash drive prices are high, you buy them when they are low. I would start aggressively accumulating Semi-Stocks over the course of 1-3 months. According to the Elliot Wave Theory, the Wave 2 selling could be coming to an end.

I was bullish on Semi land up until Jan/February of 10, when I called for a 15%-25% correction in the blog posting Watching The Leaders For A Shift. It was also this time I grew a bit bearish on the market because Semiconductors are part of the leaders in the business cycle. I was then implementing a long late cycle/short early cycle stance for hedged protection in the The Exit Strategy post and so far the strategy has worked, as we have seen late cycle commodities moving higher while semis/banks have been lackluster, with downward pressure - and that why its time to get back to Semi land, searching for entry points.

Below is a chart of MU and an Elliot Wave analysis for re-entry into that stock - overall I would be patient and wait for strategic entries back into semi-conductors, but this is where the value could be hiding, and possibly even creating superior returns to commodities for the long-term. Knowing Semi's may be in the beginning of a secular bull market, a new hedge could emerge in using Gold as a short hedge. This though would require a bit more research, as for now the Gold bull is alive and well, and juniors still present undervalued opportunities. So for the long haul, we could be setting ourselves up for a Short Gold/Long Semi strategy, at some point, but I'm not about to go there just yet.

I will also include a Mean Reversion charting technique I use to give myself another form of methodology of where/when to enter into a position.

Why Semis? And why MU - besides the fact I like the way it trades and its large liquidity, it is easily to identify its pullbacks due to its very simplistic elliott wave formation. But also, as the dollar falls, our semiconductor products and pricing become more attractive, globally. As the dollar continues to fall, or even if it stabilizes, it will be a large factor in its global competitiveness. And in the end, Semiconductors are - The Other Commodity - and remember commodities make roads and buildings - chips make everything else.

SOX COMPONENTS

ALTR,AMD,ATHR,BRCM,CREE,CRUS,HITT,INTC,KLAC,LLTC,LRCX,SNDK,STM,TER,TXN,VECO,NVDA,MU,NSM,POWI,RBCN,STM.

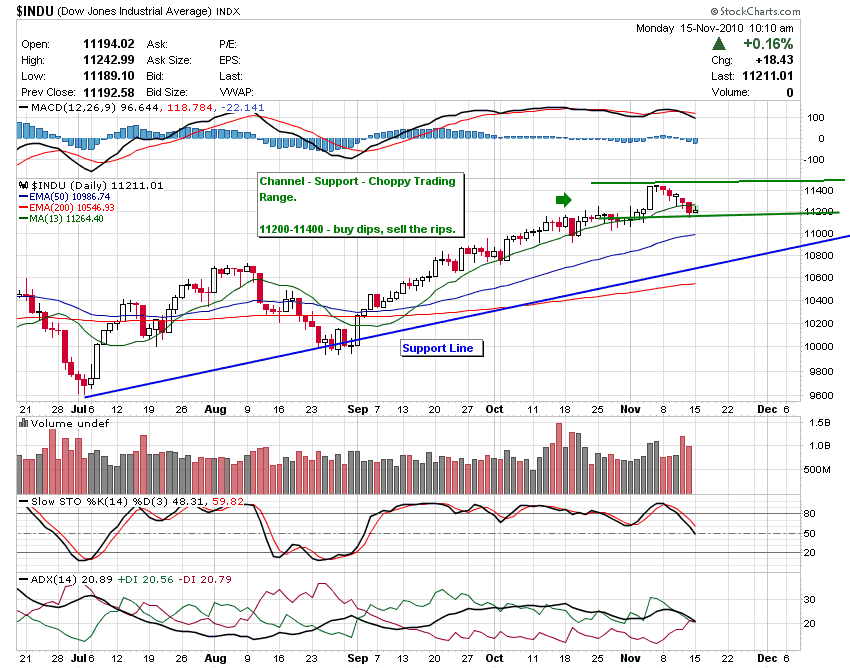

Monday, November 15, 2010

Market Stalls - Uptrend Still In Tact

The Dow Jones Industrial looked like it was going to rocket through its April/May resistance and send us in blow-off mode of some sort. That was all put by the wayside as many traders, hedge funds, algo funds, and even the small investor decided to take profits in the profit zone - meaning, anytime you come to resistance/support zones, there will be profit taking and volatility.

Looking at the DJIA and it's attempted breakout - it has now had a 5-6 day stall/correction. If we notice the large candle that gave us a signal of breaking out, and then the retracement from that candle, all of the corrective prices within that candle range. This now means DJIA has a high probability of channeling in here, before making an attempt higher or testing the current uptrend support.

Its currently a traders market with a long bias!

Looking at the DJIA and it's attempted breakout - it has now had a 5-6 day stall/correction. If we notice the large candle that gave us a signal of breaking out, and then the retracement from that candle, all of the corrective prices within that candle range. This now means DJIA has a high probability of channeling in here, before making an attempt higher or testing the current uptrend support.

Its currently a traders market with a long bias!

Thursday, November 11, 2010

Bearish Rising Wedge - GLD Intraday

Bearish Rising Wedge - Intraday GLD alert! 132 Downside target.

The risk trade is to be outright long gold here. There is need to have a hedging technique because people forget that gold is sort of useless and can fall as fast, or faster than a hyped up multi-billion dollar, no reveune, no business model, 2000 tech stock IPO. I am still a believer in the Gold bull and don't believe it's over, but I also know and realize Gold is nothing more than a measure of global psychology - the adhesive to global economics. We all share it around our neck, on our fingers, or as keepsake tokens, or maybe you have a vault with some gold bar pyramid stacked in the corner, but in the end, when the global psychology changes toward it, it will fall and fast!

A gold correction can happen faster than any algorithm can chase it, watch!!

The risk trade is to be outright long gold here. There is need to have a hedging technique because people forget that gold is sort of useless and can fall as fast, or faster than a hyped up multi-billion dollar, no reveune, no business model, 2000 tech stock IPO. I am still a believer in the Gold bull and don't believe it's over, but I also know and realize Gold is nothing more than a measure of global psychology - the adhesive to global economics. We all share it around our neck, on our fingers, or as keepsake tokens, or maybe you have a vault with some gold bar pyramid stacked in the corner, but in the end, when the global psychology changes toward it, it will fall and fast!

A gold correction can happen faster than any algorithm can chase it, watch!!

Tuesday, November 9, 2010

Bullish Engulfing Japanese Candlestick

Simple is easy - I like easy.

Here is a simple explanation of a Bullish Engulfing Japanese Candlestickpattern which is a reversal pattern - meaning a trend change. This is the DZZ - double short Gold ETF - it's a great hedge for anyone with positions in miners, tech stocks, etc. I don't believe Gold is hit its peak yet, but I do believe its corrections will become faster and more violent. Take the DZZ overnight with you for a good night sleep!

Here is a simple explanation of a Bullish Engulfing Japanese Candlestickpattern which is a reversal pattern - meaning a trend change. This is the DZZ - double short Gold ETF - it's a great hedge for anyone with positions in miners, tech stocks, etc. I don't believe Gold is hit its peak yet, but I do believe its corrections will become faster and more violent. Take the DZZ overnight with you for a good night sleep!

Saturday, November 6, 2010

AUY: A cup and handle filled with fundamentals.

With gold prices at record levels, and this new $1,000 gold quote largely accepted in the new world, AUY could be poised to make a run higher. Looking at the relative performance of the stock compared to other juniors such as KGC, AU, and GG, you can see AUY has lagged and stalled during these recent boom times in junior miners. It is showing some of the worst performance among some of it's equivalents.

3 Mines To Commence In 2012

A 3yr period of a stagnating bottom line may be about to change as Yamana plans for 3 mines to commence in 2012. The company currently produces around 1.1 million GEO's and expects that number to hover or slightly rise for 2011 as more efficiencies are constructed and worked through existing mines. It's what it expects to do in 2012 that matters - the company expects production to jump, reaching near 1.5 million GEO's by 2012 with the addition of 3 mines coming into production: C1 Santa Luz (Brazil), Mercedes (Mexico), Ernesto/Pau-Au-Pique (Brazil).

With an expected near 30% jump in production numbers coming in 12-16 months and we continue to see rising prices in gold, this makes a good case to own AUY for the long-term. Nothing has come online since 2009 in terms of Gold expansion, since the 20 month construction of Gualcamayo in Argentina. This 2012 production expansion means rising revenue. With the increase in projected gold production of 400,000 ounces, this adds nearly $500 million in revenue using an avg. price of $1,200 an ounce. This increases the current $1.4 billion in revenue(ttm) to $1.9 - 2 Billion in projected revenue, a near 35% jump in revenue.

BOOK VALUE

If we look at a simple Book Value comparison in a couple of the junior miners, we can see AUY trades at 1.22 Price to Book almost book value as of today. With GG and KGC trading at 2 and 2.23 Price to Book respectively, AUY could almost double to get where KGC and GG are trading. And to reach the relative Price to Book of AU and IVN, AUY would have to rise 2-3x in price.

BOOK VALUE COMPARISON

The Book Value and Price To Book value are telling you that AUY is undervalued and could be headed higher. Base on a possible technical formation called the Cup and Handle AUY could be headed for $15 dollars in the near term, and if we valued it at a Price to Book of 2, we'd be trading around 18. And if the market valued AUY according to an AU and IVN book value, AUY would be in the 30's, heading to $40.

The technical formation above is a continuation pattern. The trend has been up, but stalled in the past 3 years as Yamana focused on integrating new efficiencies in production, rather than new production. Now Yaman is ready to ramp up production and the last time they did this, AUY went from $2 to a high near $18 dollars from 2005 - 2008. With gold prices elevated, production getting set to rise, a book value that may be lagging its coming rising production, Yamana is set to run and possibly even jump a few times also.

3 Mines To Commence In 2012

A 3yr period of a stagnating bottom line may be about to change as Yamana plans for 3 mines to commence in 2012. The company currently produces around 1.1 million GEO's and expects that number to hover or slightly rise for 2011 as more efficiencies are constructed and worked through existing mines. It's what it expects to do in 2012 that matters - the company expects production to jump, reaching near 1.5 million GEO's by 2012 with the addition of 3 mines coming into production: C1 Santa Luz (Brazil), Mercedes (Mexico), Ernesto/Pau-Au-Pique (Brazil).

With an expected near 30% jump in production numbers coming in 12-16 months and we continue to see rising prices in gold, this makes a good case to own AUY for the long-term. Nothing has come online since 2009 in terms of Gold expansion, since the 20 month construction of Gualcamayo in Argentina. This 2012 production expansion means rising revenue. With the increase in projected gold production of 400,000 ounces, this adds nearly $500 million in revenue using an avg. price of $1,200 an ounce. This increases the current $1.4 billion in revenue(ttm) to $1.9 - 2 Billion in projected revenue, a near 35% jump in revenue.

BOOK VALUE

If we look at a simple Book Value comparison in a couple of the junior miners, we can see AUY trades at 1.22 Price to Book almost book value as of today. With GG and KGC trading at 2 and 2.23 Price to Book respectively, AUY could almost double to get where KGC and GG are trading. And to reach the relative Price to Book of AU and IVN, AUY would have to rise 2-3x in price.

BOOK VALUE COMPARISON

The Book Value and Price To Book value are telling you that AUY is undervalued and could be headed higher. Base on a possible technical formation called the Cup and Handle AUY could be headed for $15 dollars in the near term, and if we valued it at a Price to Book of 2, we'd be trading around 18. And if the market valued AUY according to an AU and IVN book value, AUY would be in the 30's, heading to $40.

The technical formation above is a continuation pattern. The trend has been up, but stalled in the past 3 years as Yamana focused on integrating new efficiencies in production, rather than new production. Now Yaman is ready to ramp up production and the last time they did this, AUY went from $2 to a high near $18 dollars from 2005 - 2008. With gold prices elevated, production getting set to rise, a book value that may be lagging its coming rising production, Yamana is set to run and possibly even jump a few times also.

Subscribe to:

Posts (Atom)